Understanding Payment Bonds

Understanding Payment Bonds Payment bonds serve a vital function in the construction industry by ensuring that subcontractors and suppliers are compensated for their work. This bond protects the interests of all parties involved in a project, as it guarantees payment regardless of the contractor's financial condition. In many states, payment bonds are legally required for public construction projects, reinforcing their importance in the industry.

Understanding Different Types of Construction Bonds

Understanding Different Types of Construction Bonds Before diving into the specifics of the bonding process, it's crucial to understand the various types of construction bonds available. The most common types include performance bonds, payment bonds, and bid bonds. Each type serves a distinct purpose and addresses different aspects of a construction project. Performance bonds ensure that the contractor completes the project as per the contract terms, while payment bonds guarantee that subcontractors and suppliers get paid for their services. Bid bonds, on the other hand, protect the project owner from losses if a contractor fails to honor their bid.

In weighing the pros and cons of implementing strategies to prevent bond claims, it is evident that the benefits often outweigh the drawbacks. While there may be initial costs and time commitments, the long-term advantages of reducing disputes and ensuring project success are invaluable. By prioritizing proactive measures, stakeholders can create a more efficient and reliable construction environment.

Utilizing Insurance as a Protective Measure

Another effective way to prevent construction bond claims is to utilize appropriate insurance coverage. Various types of insurance can protect against different risks associated with construction projects. General liability insurance, workers' compensation, and builder's risk insurance are essential coverages that can safeguard against claims arising from accidents, injuries, or property damage during construction.

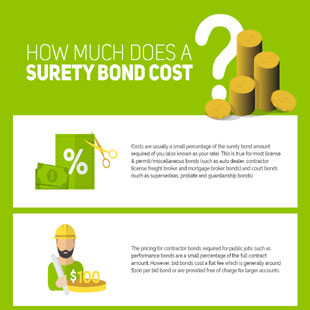

How do I obtain a construction bond?

To obtain a construction bond, you typically need to apply through a surety company. The application process involves providing financial documentation, project details, and a background check to assess your qualifications and financial stability.

Furthermore, staying informed about industry regulations and best practices is essential. The construction landscape is constantly evolving, and being aware of changes in laws, regulations, and standards can help prevent disputes. By fostering a culture of education and awareness, stakeholders can collaboratively work towards minimizing the potential for bond claims.

Financial Stability and Creditworthiness

Financial stability is a primary concern for bonding companies. When applying for a bond, expect to provide your financial statements, including balance sheets and income statements. These documents will help the bond issuer assess your creditworthiness. A robust financial standing can result in lower premiums and faster approvals.

In addition to financial statements, bonding companies may also check your credit score. A high credit score indicates reliability and trustworthiness, which can expedite the approval process. If your credit score is lower than desired, consider taking steps to improve it before applying for a construction bond.

Educating Stakeholders on Bond Claims

Education is a powerful tool in preventing construction bond claims. All parties involved in a construction project should understand their rights, responsibilities, and the implications of construction bonds. Conducting training sessions or workshops can provide stakeholders with valuable insights into bond claims, the claims process, and effective strategies for prevention.

Frequently Asked Questions

What is a surety bond, and why do I need one?

A surety bond is a contract that guarantees the fulfillment of a particular obligation, such as completing a construction project. For more perspective, see performance and payment bonds for a clear overview. It protects project owners from potential losses if a contractor fails to meet their contractual obligations.

What types of construction bonds are there?

What types of construction bonds are there?There are several types of construction bonds, including performance bonds, payment bonds, and bid bonds. Each type serves a different purpose, ensuring the completion of projects and payment to subcontractors.